International political discourse in 2025 has been haunted by the spectre of Donald Trump and his brute force reshaping of global trade relationships to the (perceived) advantage of the United States. Canadians have been consumed by the question of when a deal might be struck to end Trump’s egregious tariffs, real and threatened, and what that deal might cost us. Two deadlines for an agreement, July 21 and August 1, have passed with no clarity on what comes next, or even what’s on the negotiating table.

President Trump’s demands seem to change from day to day. Canadian concessions to the Trump agenda—including cancelling a multibillion dollar digital services tax, introducing worrying border and immigration reforms, and potential participation in a costly continental missile defence scheme—have clearly gone unnoticed or unappreciated in Washington. It’s not clear how much more capitulation Prime Minister Mark Carney is prepared to make in order to secure a deal.

No deal is better than a bad deal, as economist Jim Stanford has argued convincingly. That is especially true of a bad deal that further locks Canada into the orbit of a deeply troubling regime that views acquiescence as weakness, a sign to demand more and more. As we quickly approach the planned review of the Canada-U.S.-Mexico Agreement (CUSMA), it may be wise for both Canada and Mexico to avoid bilateral “deals” in favour of a more balanced trinational conversation about the North American economy.

In this article, we review the bewildering array of tariffs announced by the Trump regime and assess their impact so far on the Canadian economy. We then examine the “deals“ the Trump administration has reached with the United Kingdom, European Union and other U.S. trade partners, and compare this to what Trump may be demanding of Canada. Based on the breadth of the Canada-U.S. talks and the risks involved in conceding to Trump in a number of areas, we are concerned the government’s strategy appears very different from the “elbows up” slogan we heard during the election.

Status of U.S. tariffs and Canadian counter-tariffs

Amid the on-again, off-again tariff announcements spanning every country in the world (and some islands inhabited solely by birds), it can be challenging even for experts to keep track of what’s happening. There are several distinct flavours of tariffs affecting Canada-U.S. trade and U.S. trade from other countries:

- National emergency and so-called reciprocal tariffs.

- Sectoral tariffs on steel, aluminum, copper and automotive imports, with likely extension to the semiconductor, timber and lumber, trucks, commercial aircraft and pharmaceutical sectors.

- Anti-dumping and countervailing duties on softwood lumber.

- Canadian retaliatory tariffs on a list of U.S. imports, including foodstuffs, finished products and some industrial inputs.

National emergency and reciprocal tariffs

Much of the Trump administration’s justification for launching a trade war on the world stems from a 1977 law, the International Emergency Economic Powers Act (IEEPA), which grants the U.S. president authority to regulate economic transactions once a national emergency has been declared. The law was used, until now, to justify sanctions on foreign states or their governments, and more recently on individuals and non-state actors or groups.

Trump claims the IEEPA gives him the right to impose tariffs as well. One of the first actions of the new Trump administration was to impose tariffs on Canada and Mexico, based on a declared emergency related to purported imports of the opioid fentanyl and fears about immigration. This move made good on a promise Trump made shortly after the November 2024 presidential election.

Outside of North America, the IEEFA tariffs have been called “reciprocal tariffs,” as they respond to alleged foreign barriers to U.S. exporters. Trump’s initial list of reciprocal tariffs, announced on April 2, “Liberation Day,” included a minimum 10 per cent rate, with much higher tariffs for several countries. These tariffs, which were paused for 90 days following a flight from U.S. equities, treasuries and the U.S. dollar, formed the starting point for bilateral trade negotiations.

These tariffs are facing legal challenges at the World Trade Organization and from within the U.S., where the Court of International Trade and the District Court for the District of Columbia have declared them illegal, pending appeals. While ostensibly about addressing perceived trade imbalances, Trump imposed a 40 per cent tariff on all Brazilian imports for prosecuting former president Jair Bolsonaro for his role in an attempted coup.

The IEEPA tariffs were initially set at 25 per cent for Canadian exports, with a lower 10 per cent rate on energy exports—a tell that the U.S. needs a lot of what Canada sells it. The former rate was raised to 35 per cent on August 1. However, goods that qualify for tariff-free treatment under CUSMA are currently exempted from these tariffs.

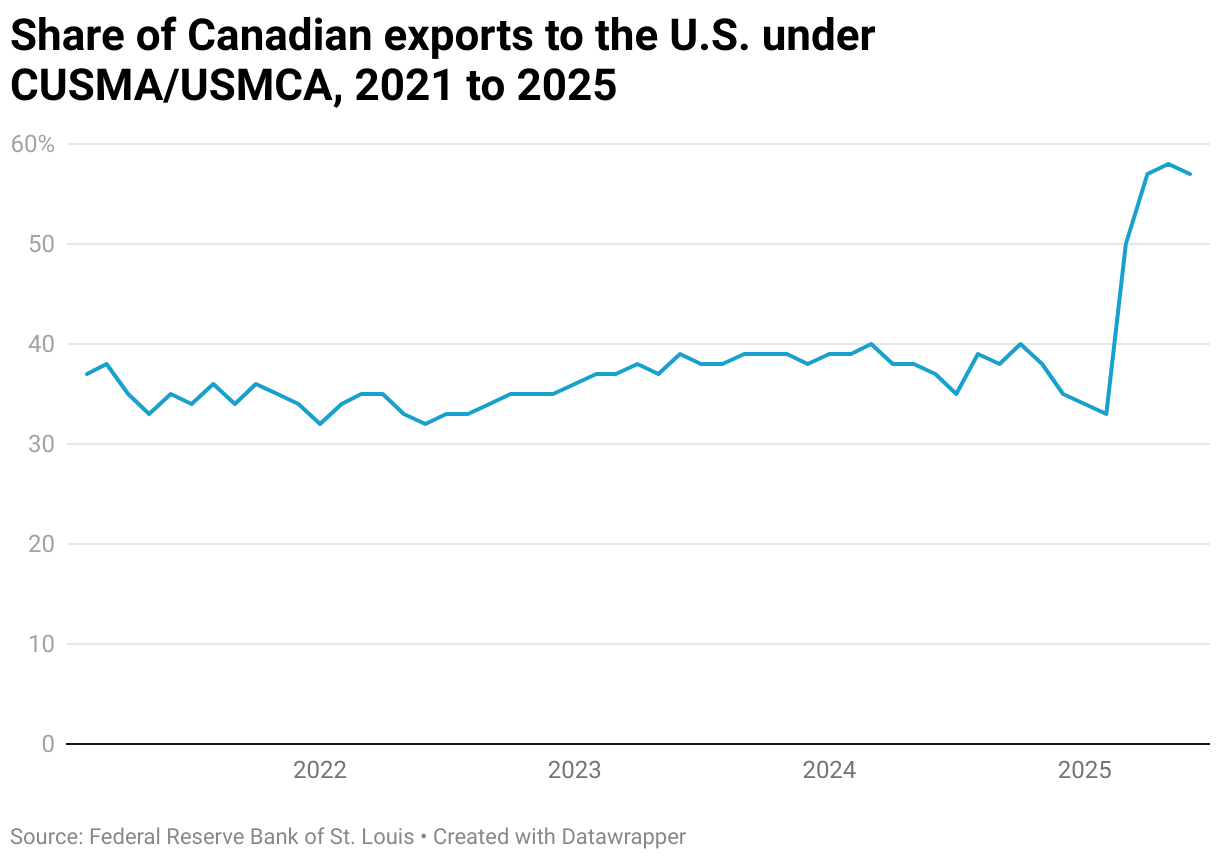

Prior to the Trump tariffs, only about 40 per cent of Canadian exports were certified as CUSMA-compliant due to the high costs and complexities of registration and compliance. As Figure 1 shows, that share shot up to 57 per cent of Canadian exports in recent months. Potentially, 90 per cent of Canada’s exports could qualify as CUSMA-compliant, although this requires additional costs for Canadian exporters. (Note this costly reality in comparison to the oft-stated line that it’s easier to trade with the U.S. than with other Canadian provinces.)

Sectoral tariffs

In addition to the IEEFA tariffs, a number of sectoral tariffs have been introduced under Section 232 of the Trade Expansion Act of 1962. The law allows the president to impose tariffs, quotas or other restrictions to imports when an investigation determines they threaten national security. These tariffs are being deployed on all countries, purportedly to induce new investment into the U.S. in covered sectors while providing Trump leverage in international trade talks.

Shortly into his first term as president, Trump imposed sectoral tariffs of 25 per cent on steel and 10 per cent on aluminum imports, then negotiated them away with Canada and Mexico during the NAFTA renegotiations that led to the CUSMA. Shortly after taking office this year, Trump issued an executive order claiming that new information justified reimposing those tariffs at a higher 25 per cent rate, raised to 50 per cent, in June, on all foreign imports. Recently, the US announced an expansion of these metal tariffs to 407 categories of “derivative” products that contain steel and aluminum, causing more uncertainty for Canadian exporters.

The Trump administration also imposed a 25 per cent Section 232 tariff on imports of all foreign automobiles, again partly based on a national security review undertaken in his first term as president. In doing so, Trump violated side-letters signed with Canada and Mexico at the close of the NAFTA renegotiations promising that a certain quota of imports from either country would be safe from future national security tariffs

Facing pressure from North American automakers, Trump moderated the 25 per cent tariff for CUSMA-compliant vehicles, which only face a 25 per cent tariff on non-U.S. content (typically about half the value of a finished vehicle assembled in Canada). Auto parts from Canada and Mexico are exempt from the 25 per cent tariff for two years. But the Trump administration has launched another Section 232 investigation into trucks and heavy-duty vehicles that could be devastating for the Canadian automotive industry.

Further to these highly damaging industry-wide tariffs, a new 50 per cent tariff was introduced on some copper products beginning August 1. The tariffs will apply to about $3 billion worth of annual semi-finished copper product exports and may eventually cover refined copper—the bulk of our U.S. exports—with a 15 per cent tariff in 2026 and 30 per cent tariff in 2027. Trump’s order directly menaces Canada’s copper manufacturing sector by shifting Canadian exports lower down the value chain.

New sectoral tariffs of up to 100 per cent on semiconductors and up to 200 per cent on pharmaceuticals are expected to be announced soon. Ongoing Section 232 investigations into trucks, the aerospace sector, and timber and lumber may result in future tariff hikes threatening Canadian workers.

Countervailing and antidumping duties on softwood lumber

Unlike Trump’s metals and automotive tariffs, U.S. concerns with Canadian lumber imports have been ongoing for more than two decades. Apart from a brief period of negotiated calm during the Obama presidency, Canadian lumber exports have often faced significant anti-dumping and countervailing duties based on allegations that stumpage rates for felling trees on Crown land are too low and therefore an unfair subsidy for Canadian exports—an argument rejected by a World Trade Organization dispute panel in 2020.

Under WTO and CUSMA rules, countries may impose tariffs/duties on imports of goods sold into their domestic market at below-market prices (anti-dumping duties) or that benefited from subsidies (countervailing duties). The Trump administration tripled the anti-dumping rate on Canadian softwood lumber in late July (to 20.56 per cent), then revised the countervailing duty rate from 6.74 per cent to 14.63 per cent in August.

That puts the combined tariff at 35.19 per cent. The Canadian forestry industry and Canadian unions representing forestry workers have called on the federal government to negotiate a long-term softwood lumber agreement with the U.S. while helping the industry to transition to more value-added production that is less dependent on access to the U.S. market. In early August, the federal government announced a package of support measures for the industry, including $700 million in loan guarantees, $500 million towards diversification and value-added production, and $50 million in income and other retraining support for workers.

Canadian retaliatory tariffs

Canada responded in March and April with retaliatory tariffs of 25 per cent across a wide range of U.S. imports. These comprise many agricultural commodities (e.g. meat, vegetables, beverages, tobacco), raw materials (e.g. plastics, rubber, wood, paper), clothing and textiles, vehicles, electronics, tools and machinery and equipment. In virtually all cases, Canadian or non-U.S. alternatives are available for all of these tariffed goods. Some Canadian provinces have also taken U.S.-made liquor off shelves.

Canada also initially imposed reciprocal tariffs of 25 per cent on steel, aluminum and non-CUSMA-compliant automobiles. However, a remissions program for tariffs paid on steel and aluminum that is transformed into other goods in Canada has significantly watered down the initial retaliation, based on industry concerns about availability of affordable non-U.S. alternatives (e.g., for beer and tomato cans). Canada has exempted automotive tariffs for companies that commit to producing vehicles in Canada and has not matched Trump’s increase to 50 per cent tariffs for steel and aluminum.

Recently, the federal government announced it will remove the retaliatory tariffs on CUSMA-compliant goods by September 1. At the same time, these tariffs netted the government $2.4 billion in customs revenues in April and May, partially offsetting weaker corporate and sales taxes from the tariff-induced economic slowdown. Some of this new money is being used to support workers and industry in impacted sectors, including forestry and steel. Canada has also introduced steel import caps and tariffs on non-U.S. imports, including from free trade partners, in an effort to protect struggling domestic producers.

Economic impacts and trade data

All of the above tariff measures naturally affect the Canadian economy in direct and more complicated ways. As of early August, there’s good news and bad news for Canada. Overall, Canada’s economy has held up reasonably well in light of the circumstances. Economic activity, including trade, ramped up at the end of 2024 and early 2025, the period before new tariffs were implemented, then swung the other way in the second quarter.

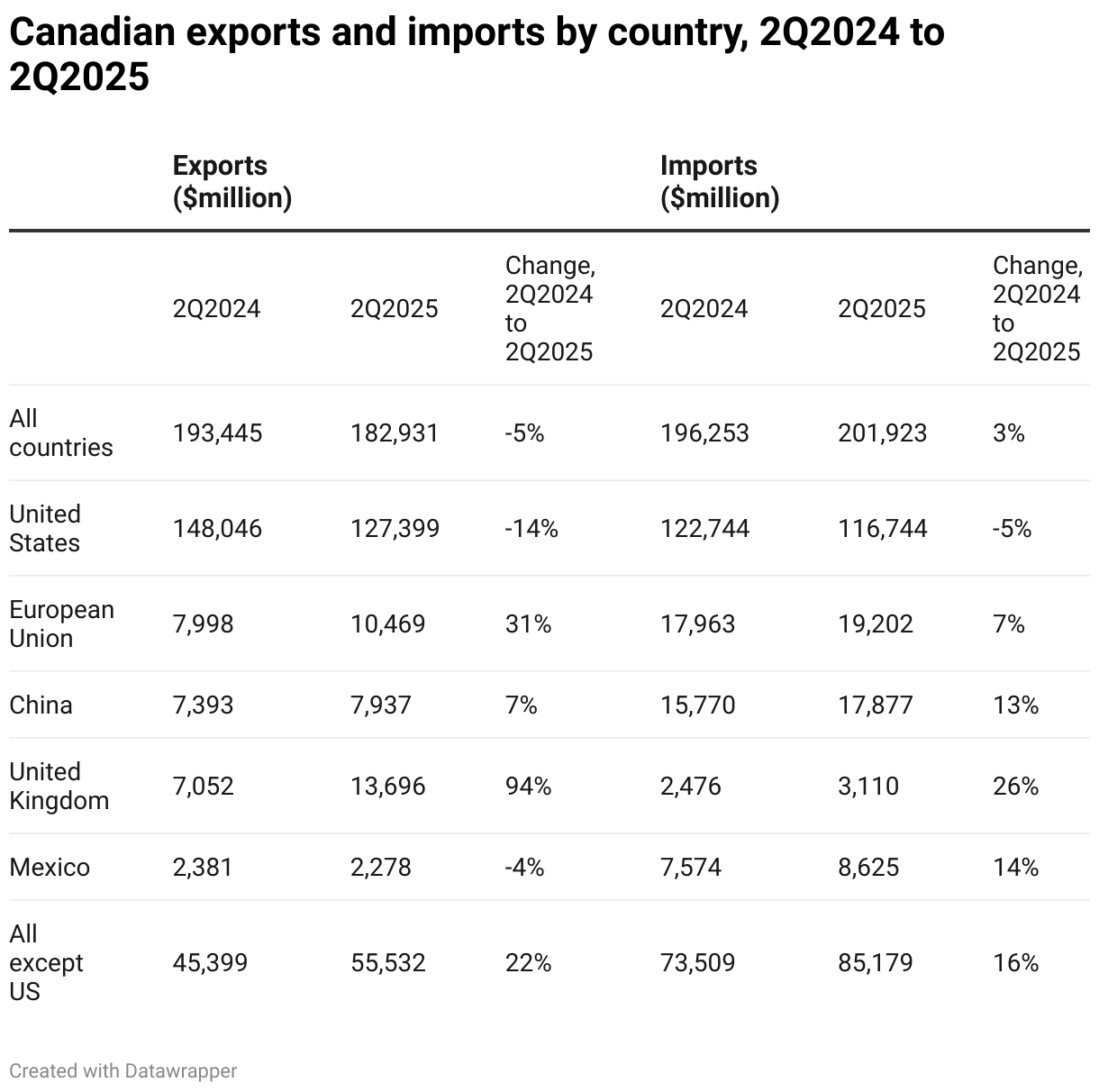

Canada’s merchandise trade balance has swung sharply negative in the wake of the Trump tariff war. In the second quarter of 2025 (2Q2025), Canada’s merchandise trade deficit was just under $19 billion compared to just under $3 billion in the second quarter of 2024 (2Q2024). This comes after a surge in U.S.-bound exports in the first quarter of 2025 as exporters tried to get ahead of the looming tariffs. Table 1 shows that overall exports fell by five per cent in 2Q2025 over 2Q2024, led by declining exports to the U.S. of 14 per cent, while overall imports increased by three per cent, but imports from the U.S. fell by five per cent.

In recent years, Canada has had roughly balanced merchandise trade, with surpluses on U.S. trade offset by deficits on trade with the rest of the world. The deteriorating trade balance reflects a much smaller trade surplus with the U.S., at a seasonally adjusted $25.3 billion in 2Q2025 compared to $10.7 billion in 2Q2024. Canada’s trade deficit with the rest of the world has been fairly stable through 2025. Note that these numbers do not count services trade, which had a small $3 billion deficit for the first half of 2025.

Looking just at merchandise exports, the good news is that exports to the United Kingdom and European Union surged by 94 per cent and 31 per cent respectively in 2Q2025 over 2Q2024—a combined increase of $9 billion—thereby offsetting some of the $20.6 billion decrease in exports to the U.S. The starting points are admittedly very different, as exports to the U.S. are more than four times greater than exports to the U.K. and Europe combined. Still, this points to the promise of trade diversification, although it will take some time to change trading patterns. Set against this, Canada’s trade balances with both China and Mexico worsened in 2Q2025 compared to 2Q2024.

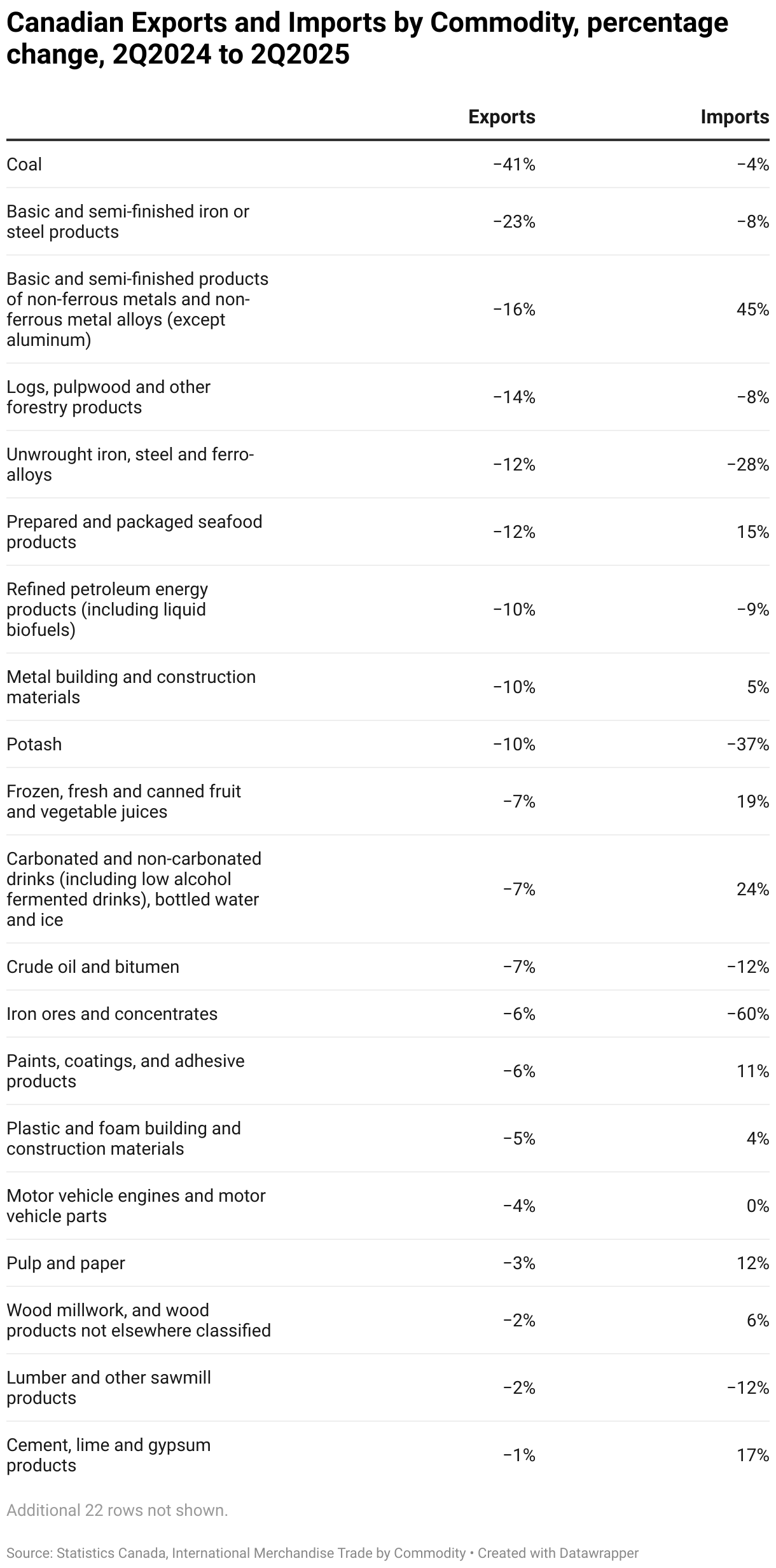

Trade statistics for a wide range of exported commodities, showing the change in exports by value in 2Q2025 compared to 2Q2024, are shown in Table 2. These include exports to all countries, not just the United States, and are in dollar values, meaning some of the change for basic commodities may be due to prices rather than quantities. Outside of the areas affected by the sectoral tariffs, export volumes have generally held their own, and, in some cases, actually increased. The large drop in coal exports is primarily due to the fall in world prices for coal (Canadian coal is largely exported to Asia, not the U.S.).

However, Canadian exports affected by the U.S. sectoral tariffs were all down substantially in 2Q2025 compared to a year earlier. This included exports of basic and semi-finished iron or steel products, down 23 per cent, basic and semi-finished products of non-ferrous metals and non-ferrous metal alloys (except aluminum), down 16 per cent, logs, pulpwood and other forestry products, down 14 per cent, and unwrought iron, steel and ferro-alloys, down 12 per cent (on a value basis). Metal building and construction materials exports are also down 10 per cent year over year. Lumber and other sawmill product exports are down two per cent (although monthly numbers for June show further deterioration).

In the auto sector, exports of passenger cars and light truck exports held steady (but were down 16 per cent in June compared to June 2024) while exports of motor vehicle engines and motor vehicle parts were down four per cent.

The downturns in each sector have produced job losses and temporary work shutdowns, which we can notice in relatively higher unemployment rates in manufacturing and forestry communities. These statistics highlight the need to support workers in the core areas affected by tariffs. At the same time, the narrower impact on more export-dependent sectors means the federal government can provide assistance to those sectors without massive costs to the treasury. The recent announcement of $1.2 billion in federal support for the softwood lumber industry is a good case in point.

Nonetheless, Donald Trump‘s strategy of reducing its trade deficit through tariffs is basically working in the case of Canada. Whether it is successful in inducing new investments in the U.S. to avert the tariffs remains to be seen.

Moreover, it appears the other shoe is about to drop in the United States. Higher prices from tariffs, a downturn in housing, deep cuts to the public sector, and the overall uncertainty brought about by the Trump regime all point to a worsening U.S. economy, with rising unemployment. While it is still too early to tell the full economic impact in the U.S., Canada and other countries affected by the tariff war, estimates of the likely impact of U.S. tariffs on consumer prices should be read as a longer-term warning and not as immediate reality.

The art of the deals

Countries around the world have been rattled by the rollercoaster of tariff announcements from the White House. Most countries have launched negotiations with the U.S. to lower their “reciprocal” tariff rates, and a few high-profile deals have been announced.

For the most part, these deals have been more limited and transactional. They are more like non-binding memoranda of understanding, and very different from actual trade agreements that can run hundreds of pages long. And for all of the media coverage, none of these deals have been implemented so far, keeping countries in the limbo of uncertainty in the short term, but also anxious about when another set of demands from Trump will arrive.

United Kingdom: Announced in May, the U.K.-U.S. Economic Prosperity Deal is a limited tariff deal with a commitment to keep talking about so-called no-tariff barriers to trade. Key ingredients include lower tariffs on U.K. exports of cars (10 per cent instead of the global 25 per cent rate), steel and aluminum (25 per cent versus 50 per cent), while the U.K. removes existing tariffs on beef and ethanol imports from the U.S. The two countries continue to discuss an arrangement covering aerospace and pharmaceuticals.

European Union: In late July, a trade deal with the EU was announced that includes a maximum 15 per cent tariff across the board for EU exports including cars, pharmaceuticals, chips and lumber but not steel and aluminium, which remain at 50 per cent tariffs. The EU removes tariffs on industrial goods and provides better market access for fish and certain agricultural goods. The EU also committed to purchase US$750 billion American LNG over the next three years—a physically impossible feat given dropping demand for gas on the continent.

Japan: In July, the U.S. and Japan agreed to a strategic trade agreement. The deal subjects Japan to a 15 per cent baseline tariff and also provides for US$550 billion in Japanese investment in U.S. the energy, semiconductor, critical minerals, pharmaceuticals, and ship building sectors. The 15 per cent tariff covers automobiles, putting Japanese producers at a competitive advantage relative to Canadian-made vehicles. As in the E.U. deal, steel and aluminum tariffs remain elevated for Japanese producers. U.S. exporters get improved market access for agricultural commodities, energy, manufacturing, aerospace, automobiles and industrial goods, at least on paper. There has been some dispute about the details of the trade deal, with the two sides out of alignment on how the Japanese investments will be structured (e.g., as a loan or loan guarantees, or as direct investment).

China: The U.S. does not have a deal with China, but President Trump’s main preoccupation concerns the U.S. trade deficit with the “world’s factory.” Proposed U.S. tariffs on Chinese goods of up to 145 per cent hang over the talks, though Chinese imports currently face a 34 per cent tariff and U.S. exports to China face a 10 per cent retaliatory tariff (down from a proposed 125 per cent). China has also imposed retaliatory tariffs on Canadian agricultural and seafood products in response to Canadian tariffs of 100 per cent on electric vehicles,which emulated U.S. actions taken under the Biden administration and were implemented in October 2024.

What’s on the table for Canada?

While countries that have struck deals with Trump have largely focused on transactional arrangements that accept a lower tariff, Canada has gone the other direction by seeking to roll security into a broader deal that may prove expensive but without guarantees of market access. For example, Trump has said Canada could participate in the latest iteration of the U.S. missile defence scheme (previously called “star wars” now referred to as the “golden dome”), if it is willing to pony up $100 billion.

Prime Minister Carney does not appear to be rushing the U.S. negotiations, but the Canadian government response so far leaves much to be desired. The federal and provincial panic about fixing internal trade made for good headlines, but as we have pointed out elsewhere, it is mostly political theatre. A push for new national infrastructure has run up against resistance from First Nations and environmental activists due to its apparent fossil fuel-heavy orientation. The government’s promise to ramp up defence spending will be paid out of economically and socially harmful cuts to other government programs and services.

The CUSMA also is up for renegotiation in 2026, so the federal government faces more time at the trade negotiations table even if it can secure a temporary arrangement with Trump. A May 2024 CCPA report proposed that Canada’s best strategy in any CUSMA review was to boldly propose a number of changes to the deal that would benefit workers in all three countries.

In advance of any deal, Canada has already made concessions to the U.S. In July, Canada pulled its digital services tax that was on the cusp of implementation, a massive gift to U.S. tech corporations and billionaires. Canada has also promised a massive increase in military spending, eventually reaching five per cent of GDP. As the CCPA has pointed out, spending cuts to transfers and programs that matter for Canadians are likely the consequences of this military ramp-up, along with higher federal debt. Canada has also beefed up border security in response to the national emergency tariffs.

Prime Minister Carney has kept his strategy cloaked from the public. It is not clear who the Prime Minister’s Office is consulting, what Canada has offered to Trump, or what Trump may be demanding. Other unrelated domestic and foreign policy announcements also risk the ire of Trump, such as Carney’s call that Canada would recognize a Palestinian state in September, which was immediately met with hostility by Trump, who linked it to the trade negotiations.

In terms of economic concessions, two major areas may be on the table to secure a deal: critical minerals and agricultural supply management programs. And even with such concessions, Canada may still face (reduced) tariffs on a large share of exports to the U.S.

Critical minerals: While Ontario Premier Doug Ford bemoaned Trump’s “betrayal” of Canada, his proposal for a Fortress Am-Can, in which Canadian metals, minerals and energy continue to power U.S. economic and military might has support from many in the business sector. These offers are tied to deregulatory efforts in Ontario and at the federal level, which are intended to entice domestic and foreign investment into new fossil fuel and extractive projects, including Ontario’s “Ring of Fire.” It’s possible the U.S. would request first right of investment (profits) or access to Canadian deposits of materials critical to U.S. defence production (the U.S. Department of Defense is already an investor in Canadian mines) while restricting Canada’s ability to move resources up the value chain through domestic upgrading and processing.

Supply management. The program large U.S. dairy producers (and Canadian conservatives) love to hate manages Canadian production in dairy, eggs and poultry, and is always on the hit list in Canada-U.S. trade talks. Currently, U.S. imports are allowed, tariff free, up to a specified limit, above which they face steep tariffs. However, U.S. producers feel they are being shut out of their full allowance by Canadian importers, who are largely made up of Canadian dairy processors. The U.S. twice challenged this tariff-rate-quote (TRQ) regime under the CUSMA dispute settlement process and won concessions from the federal government, though the dispute panels underlined Canada’s right to manage the dairy import regime as it saw fit.

It is not clear what any new trade and security deal is worth with such a volatile U.S. president who will clearly resort to tariffs to exert leverage in any future situation that displeases him, including additional retaliatory tariffs Canada may be considering. Diversifying our trade relationships away from the U.S. should be a medium-term goal rather than something that can happen right away.

Mexico and Canada do not currently do a lot of trade and much of that trade, particularly in automotive goods, is weighted heavily in Mexico’s favour. With Trump’s pharmaceutical and semiconductor tariffs coming into place soon, Canada and Mexico can coordinate to reinforce Mexico’s industrial policy (full design to fab in semiconductors) and supply Mexico with cheaper generic versions of essential medicines.

Mexico, which imports most of its softwood lumber needs from the U.S., may even be open to buying more Canadian products. In so many ways, the Mexico-Canada trade and intercultural relationship is untapped and could be strengthened during our shared emergency with the United States. Coordinating with Mexico is a good idea.

There is much Canada can do in keeping with the “elbows up” vibe, with large potential to strengthen, rather than only protect, our economy from U.S. economic imperialism. This includes deepening investment in Canadian public services, strengthening Canadian ownership in the resource and core manufacturing sectors, further developing secondary manufacturing, and expanding key infrastructure in Canada with sourcing of Canadian steel, aluminum and other resources.

Stronger measures that would challenge U.S. economic interests in Canada include imposition of export taxes or other restrictions on energy and resources, a prohibition (perhaps on environmental grounds) of thermal coal exports from B.C. ports, revising the digital services tax, refusing to recognize U.S. intellectual property rights where there is a public interest reason to do so, and other retaliatory tariffs in the event of a Trump escalation.

All of these potential actions are reminiscent of the great debates over economic development, foreign ownership and over-reliance on the U.S. that took place in Canada in the 1960s and 1970s before Canada’s policy discourse was taken over by free trade. At this pivotal moment in time, reverting to the status quo of 2024, although much desired by Canadian businesses, is a fleeting fantasy. It’s time for Canada to raise its elbows to reassert its sovereignty, not bend the knee.