Budget 2025 featured talk of “generational investments” and proclaimed a headline number of $1 trillion in combined new public and private investment over five years. Yet no one seems particularly inspired by this budget or its investment plan. Let’s take a look at why it feels so underwhelming relative to the existential moment we are in.

Investment figures in the budget in several ways: so-called “generational investments” in defence, housing and public infrastructure; a shift in how the budget views public capital vs operating spending; and a more conventional, neoliberal plan aimed at spurring private investment with tax breaks while cutting red tape that is allegedly plaguing Canada’s resource export industries (reality check: crude oil exports hit an all-time high in August).

Not all investment is the same. Beyond aggregate numbers, big investments should move us closer to the country we want to be. Sovereignty, sustainability, resilience and inclusion all need to sit at the investment table. And that’s perhaps the biggest problem with budget 2025’s “all of the above” push for investment: it lacks a compelling vision of what Canada could be, and if anything, locks us into fossil fuel production for decades to come.

Capital vs operating spending

Prime Minister Carney has been reframing federal expenditures to distinguish between capital investment and operating spending. This is already the practice in B.C. (where I live), and the B.C. budget details major capital expenditures, which are then expensed over multiple years in the operating budget. These tables are also presented in a consistent annual reporting format, something the federal government should emulate.

In the federal case, the budget’s framing is that capital expenditures or public investment is good, while operating spending is more like consumption and, thus, bad. In practice, it’s tricky to make this distinction, as most public services are, one way or the other, investments in people. Education, for example, involves spending money on teachers, but that is simultaneously an investment in the students. Health care spending also has investment-like features that manifest as better economic performance, as well as overall population health. But it’s not obvious why the federal budget should be biased towards capital spending on new hospitals while ignoring the salaries (operating cost) of the professionals who work there.

In any event, this difference between capital and operating is more of a communications exercise than a pragmatic reworking of the federal accounts. The presentation of the budget projections and the fiscal plan does not change from previous budgets. Instead, an annex at the back of the budget discusses a number of categories where federal spending or tax incentives are deemed to support public and private investment. This is broadly defined, and somewhat arbitrary, but allows things like capital transfers to the provinces and R&D tax credits to be reclassified as capital.

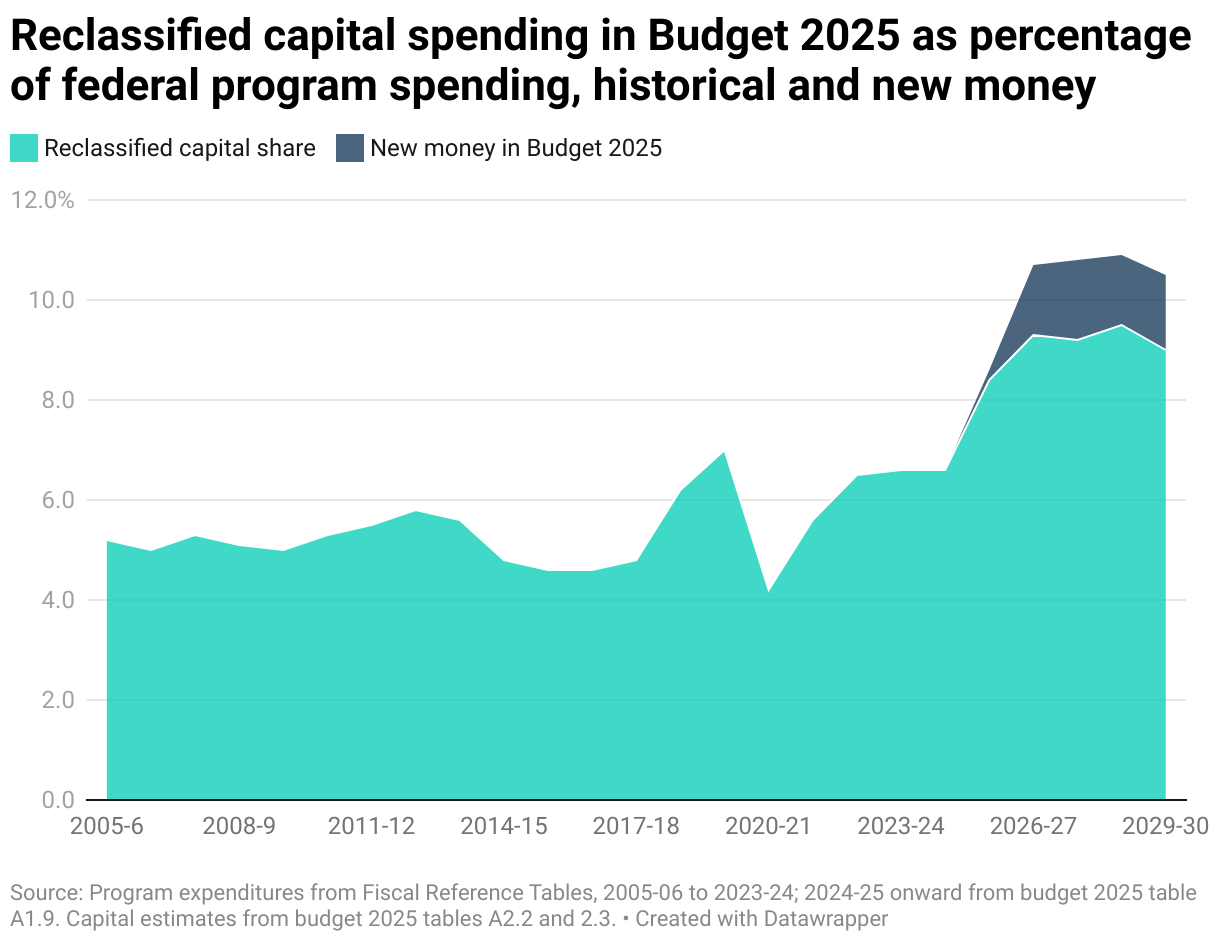

The resulting operating-to-capital shift is not particularly large. Historical data in the annex show that federal capital spending averaged 5.1 per cent of program expenditures from 2005-06 to 2017-18, and as Figure 1 shows, since then has risen to about 6.6 per cent. Budget 2025 pushes that share closer to 11 per cent within a couple years, but the vast majority of that was already planned.

Budget 2025’s capital contribution is actually rather modest: an increase of about $8 billion per year in new money, starting in 2026-27 compared to program expenditure of $528 billion that year.

This navel-gazing exercise generates a talking point for the federal government: that the operating budget will be balanced as of 2028-29, with the remaining deficit that year fully attributable to capital spending. It also creates a lens through which proposed federal initiatives and activities will be viewed in the future. Such arbitrary distinctions are also likely to have gendered implications given a more female workforce in the public sector and social services.

Ultimately, this framing helps safeguard fiscal policy from deficit hawks. It is a fairly sophisticated way of justifying necessary federal deficits in the short- to medium-term. Based on reactions to the budget, Bay Street does not seem particularly perturbed about the nation’s finances.

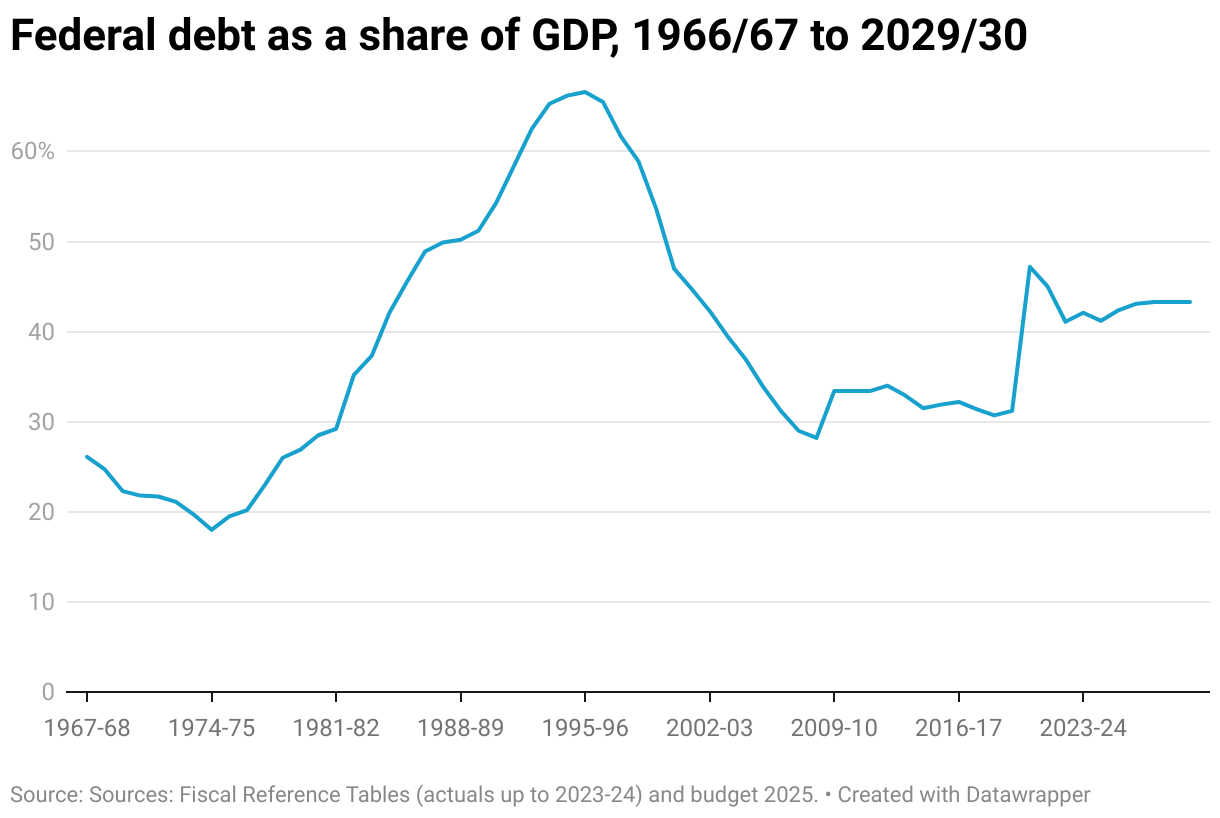

In terms of overall fiscal impact of the budget, the federal debt in relation to the size of the economy, or debt-to-GDP ratio, is what matters—and would be the same value no matter how the budget carves up capital vs operating spending. As Figure 2 shows, federal debt is down from its COVID-19 peak of 47.2 per cent of GDP in 2020-21 to 42.3 per cent in 2025-26; it is forecast to creep up to 43.3 per cent in 2027-28 and remain steady over the remaining five-year outlook.

On this scale, it does not look like the feds are massively borrowing in order to make generational investments. At the height of deficit mania in the mid-1990s, debt-to-GDP peaked at 66.6 per cent, suggesting much more room for bona fide generational investments. Remember, Canada’s economy is north of $3.2 trillion per year.

In light of existential threats from the south, we need the federal government to step up as a major player in redirecting resources to pivot our economy—not take a step back. And yet, the size of the federal government will shrink over the coming five years. Both revenues and expenditures as a share of GDP fall over the five-year forecast (from 16.6 per cent and 15.9 per cent respectively. In 2024-25, it will fall to 15.8 per cent and 15.4 per cent in 2029-30.

About those generational investments

Four buckets of “generational investment”—ostensibly totalling to $280 billion over the next five years—are the centrepiece of the budget: defence and security; housing; infrastructure; and productivity and competitiveness. However, it’s not all new money and the budget is silent on a lot of the pertinent details.

The crude trade-off in the budget is increased defence and border security spending, which is set against cuts to other federal departments. Defence-related investment is flagged at $30 billion over five years. Exactly how this plays out is not super clear, as the budget allocates money into a number of funds that will support different objectives, all of which lack specifics. There will clearly be benefits to Canadian aerospace companies and other suppliers, and hopefully a focus on dual use for defence expenditures, such as planes that help us fight summer wildfires or equipment that helps address major floods.

Housing investment largely rests on the new Build Canada Homes (BCH) program launched in September. BCH has much potential as a model of public-led development, with use of modularized construction to build energy-efficient homes. However, only about $6.5 billion in new money over five years is allocated in budget 2025. The rest of the headline housing investment of $25 billion over five years is a carryover from previous budgets, plus the value of the cut in GST for first-time buyers of new homes.

Scale is the big question mark for BCH. In terms of numbers of homes, BCH is more of a pilot program than a generational investment. The 4,000 homes to be started under BCH next year is small potatoes relative to needs. By the Alternative Federal Budget’s estimation, Canada needs about a million new non-market homes over a decade to address backlogs and accommodate population growth.

Infrastructure investment is ostensibly $115 billion over five years, but most of this is from previous budgets, not new money. Of this, $20 billion is for “generational” infrastructure investments but only $9 billion is new money (and most of it will require cost-matching from the provinces or territories). Within this envelope is a new Build Communities Strong Fund, starting in 2026-27, which continues the various streams of infrastructure spending that have been ongoing since 2016, and rolls in the Housing Infrastructure Fund announced in the 2024 budget and Canada Community Building Fund (formerly the Gas Tax Fund).

The final investment category, productivity and competitiveness, includes various incentives for private sector investment, with most of this re-announcing previous funding and very little of this is new money. For example, the extension of tax credits for R&D accounts for $27 billion of the headline investment commitment over five years but the 2025 budget enhancement to the R&D credit is only worth about $0.3 billion of this.

The federal government is implementing what it calls a “productivity super deduction”, at a cost of $1.5 billion over five years. This measure pools a number of existing tax credits aimed at allowing companies to write off big investments more quickly. Manufacturing and processing buildings get immediate expensing for new investments, while a credit for liquified natural gas (LNG) operations provides an accelerated capital cost allowance (both measures continue previous budgetary measures).

This push for faster write-offs of capital spending is consistent with the tax literature, much of which favours shifting corporate taxation to a full cash flow basis. This would allow capital expenses to be written off in the year that they are spent rather than amortized over many more years, thus better reflecting the actual operations of corporations.

Whether these actually “supercharge growth”, as claimed in the budget, is not obvious. Canada already has quite low corporate taxes, so these measures don’t necessarily translate into actual new investment, which is based on a lot of other factors, including access to raw materials and markets and labour.

Disappointingly, the budget doubles down on Canada’s historical role as an exporter of raw materials. Historically, Canada sought to overcome this in the development of more advanced manufacturing capabilities–industries now under direct threat from Trump.

Canada has also aimed to shift the investment balance in the name of climate action. That’s what carbon pricing was all about: precipitating a shift in new investment into renewable and clean alternatives rather than fossil fuels. In the name of “climate competitiveness”, however, the feds are proposing to eliminate their emissions cap for the oil and gas sector, a major step backward. Instead, action would rely on advances in industrial carbon pricing after 2030 and commitments from the provinces to support other aspects of federal action.

Perhaps the most innovative move in the budget is in the area of critical minerals. The federal government will create a sovereign fund of $2 billion, which would ostensibly allow it to take equity stakes and build supply chain infrastructure associated with new projects. There is not much detail to go on but,overall, it should be preferable to the subsidy approach we see in so many other areas.

Elbows up

After months of big talk, Canadians finally got a more concrete look at an economic plan and roadmap for how the country will meet the current political moment. And yet it’s hard to find a compelling vision of what we want to invest towards. The budget contains no major projects that feel like generational investments. Yes, there were some positive moves that continue federal infrastructure spending, but we’re not exactly swinging for the fences.

Budgets matter because that is where we show, with cold hard cash, what our real priorities are. More than any budget in the past decade, this one leans on economics and prioritizes investment. Unlocking $1 trillion in new investment over five years will require a lot of take-up on the new federal incentives and public investments.

Lost in all of this is any sort of vision for the Canadian economy. Instead, it’s an “all of the above” strategy while simultaneously downplaying other social expenditures that matter to our standard of living.

As a result, budget 2025 comes across as underwhelming. Where’s the moon shot, the national project(s) that Canadians can rally behind? Let’s end homelessness and build a million units of affordable housing, transform mobility through coast-to-coast high-speed rail network and public transit expansion, or connect provinces with an east-west electricity grid.

Instead, we are getting more export-oriented fossil fuel and mining projects. While the federal budget emphasizes longer-term prosperity through stronger investment frameworks, it’s still riddled with the same contradictions that have been facing Canadian policy for a decade, such as the need to reduce greenhouse gas emissions while simultaneously promoting the expansion of the industry that’s causing the problem.

Going forward, the federal government needs to steal more ideas from our Elbows Up compendium, which is aimed at developing a vision and approach to Canadian sovereignty that meets the times we live in.