Affordability discontent dominates Canada’s political and economic landscape—it was rated the top issue in politics as we rang in 2024 and remained in the lead throughout the year. Yet, GDP growth has exceeded expectations and average wages finally grew enough to outpace the general rise in prices during peak inflation.

How can we square this widespread anguish with seemingly positive economic indicators? Many commentators have mistakenly concluded that the source of this frustration is psychological, that common perceptions of the economy are just out of sync with the big-picture reality. They’ve even made a term for it—the so-called vibecession. The economy is doing well, they say—people are just upset because the “vibes” are off.

To people who advocate this perspective, the dominant mood is purely political, reflecting the success of right-wing populist rhetoric rather than concrete economic conditions. Those dismissive critics are missing the big picture.

The growing burden of covering basic needs

If real wages are finally recovering from the worst of the inflationary crisis, why are so many people still struggling to make ends meet? The heart of the matter is that households are forced to spend a larger share of their disposable income on essentials compared to a few years ago.

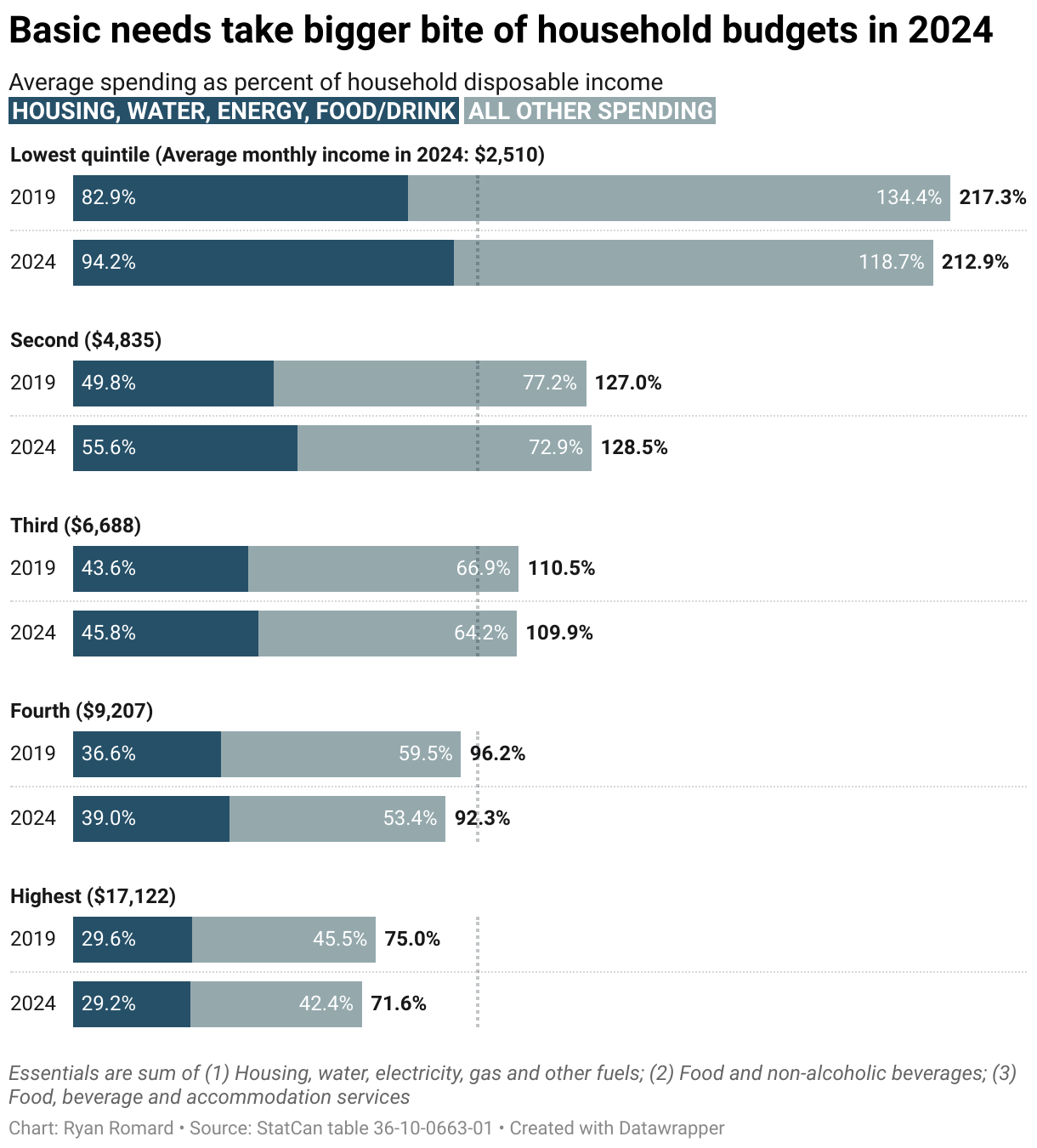

The chart below depicts average household spending as a share of household disposable income. To account for income inequality, Statistics Canada has broken the data down by income quintile, meaning five equally sized groups of households from the lowest to highest incomes.

Spending has been broken down into expenditures to meet basic needs (including housing, water, energy, food and non-alcoholic beverages) and all other goods and services. The share of income taken up by basic needs has grown for all households but those at the very top of the income hierarchy.

For households in the lowest fifth of incomes, spending on necessities rose by over 11.3 per cent, consuming nearly all of their disposable income—a deeply troubling indicator. Households in the second (5.8 per cent), third (2.2 per cent) and fourth (2.4 per cent) quintiles also experienced a rising share of income going toward necessities, with basic needs consuming between 55 and 39 per cent of their disposable income.

People in three of five income quintiles spent over 100 per cent of their disposable income in total, indicating consumption financed by debt or savings. On the other hand, high income households were spending a bit less of their total disposable income than five years ago, meaning they have more discretionary income to spend, save, or invest at the end of the month.

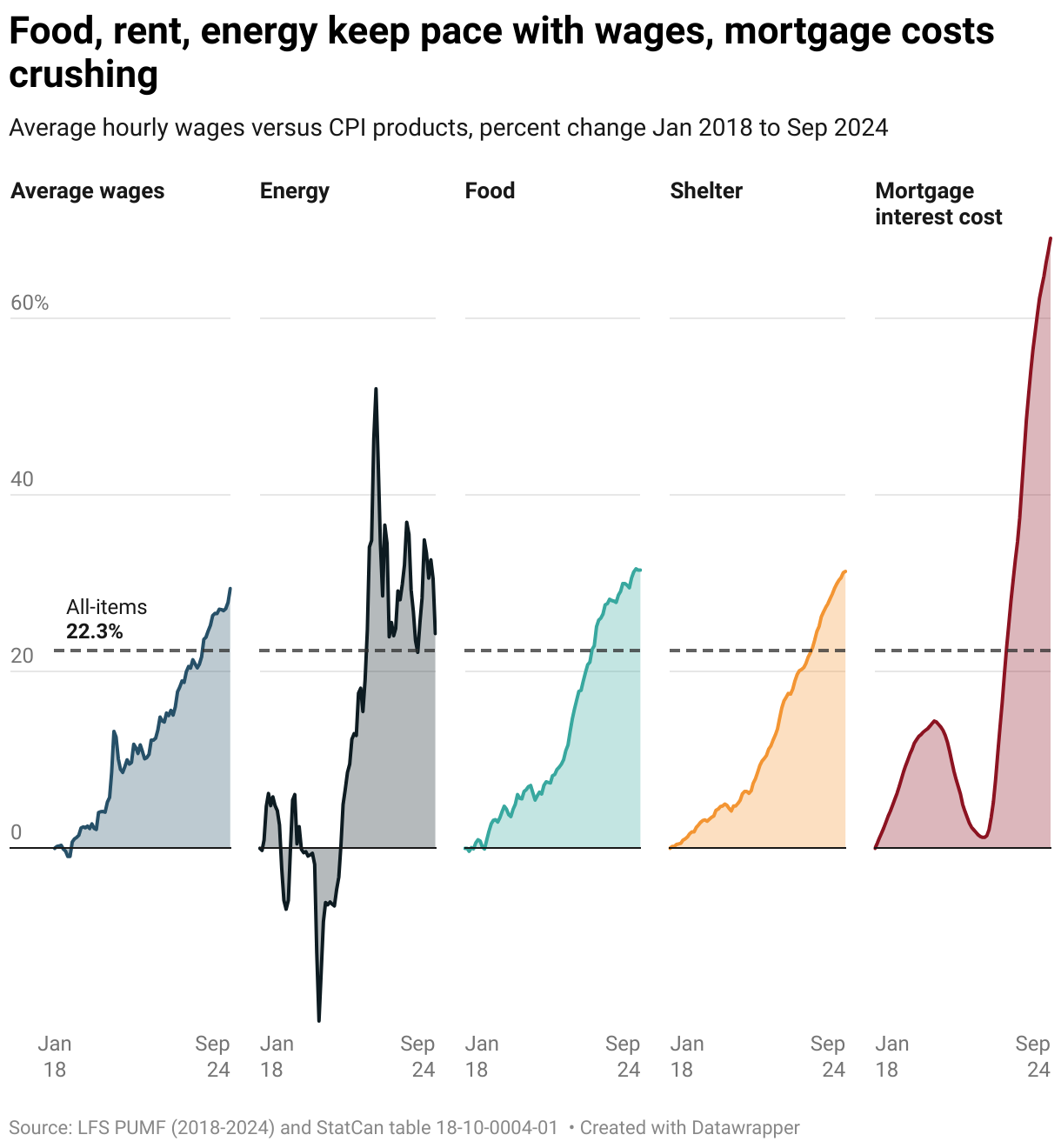

How can we explain this trend? There are two factors working together to squeeze household finances for the majority of people. The first is the most obvious, because we notice it every time we shop for groceries—prices for staple goods have grown right alongside wages, even as overall inflation falls.

Energy, food and shelter are neck-and-neck with growing wages

When most economists adjust wage data to inflation, they account for price changes using an “all-items” Consumer Price Index (CPI) that represents a typical basket of goods and services. This broad measure fails to capture disproportionate price changes in necessities that consumers feel more directly.

Since the start of 2018, average nominal hourly wages have grown by just under 30 per cent, while the all-items CPI grew by 22.3 per cent. Does this mean that wages have finally beaten inflation? Not exactly. While wage growth outpaced the broad CPI, essentials like energy and food saw sharper price increases, hitting lower-income households hardest.

The cost-of-living crisis is driven by significant price increases in a few key products, which have kept pace with wage growth even as the all-items CPI slowed. From the start of 2018 to the fall of 2024, price growth for energy outran the all-items inflation measure by two per cent, shelter by 9.1 per cent, and food by 9.2 per cent. Meanwhile, mortgage interest costs have surged by a staggering 46.8 per cent, putting home owners under immense pressure to keep up.

While energy prices have come down from the extreme heights seen in 2022, we can see from the chart above that they are still quite volatile and have been prone to rapid upticks, then steep falls in the last few years. Meanwhile, prices for food and shelter have both outpaced wage growth by about two per cent.

An extreme rise in mortgage interest costs points us toward the second major contributing factor—a generational increase in interest rates has caused the costs of carrying debt to skyrocket.

Rising interest rates are squeezing households–as intended

For decades, low interest rates kept the burden of debt repayment in check. Since the cost of living crisis accelerated with the increased inflation levels of 2021-2022, people have relied more on debt to fund their consumption. At the same time, the once very manageable costs of holding debt have surged to levels not seen in over 30 years.

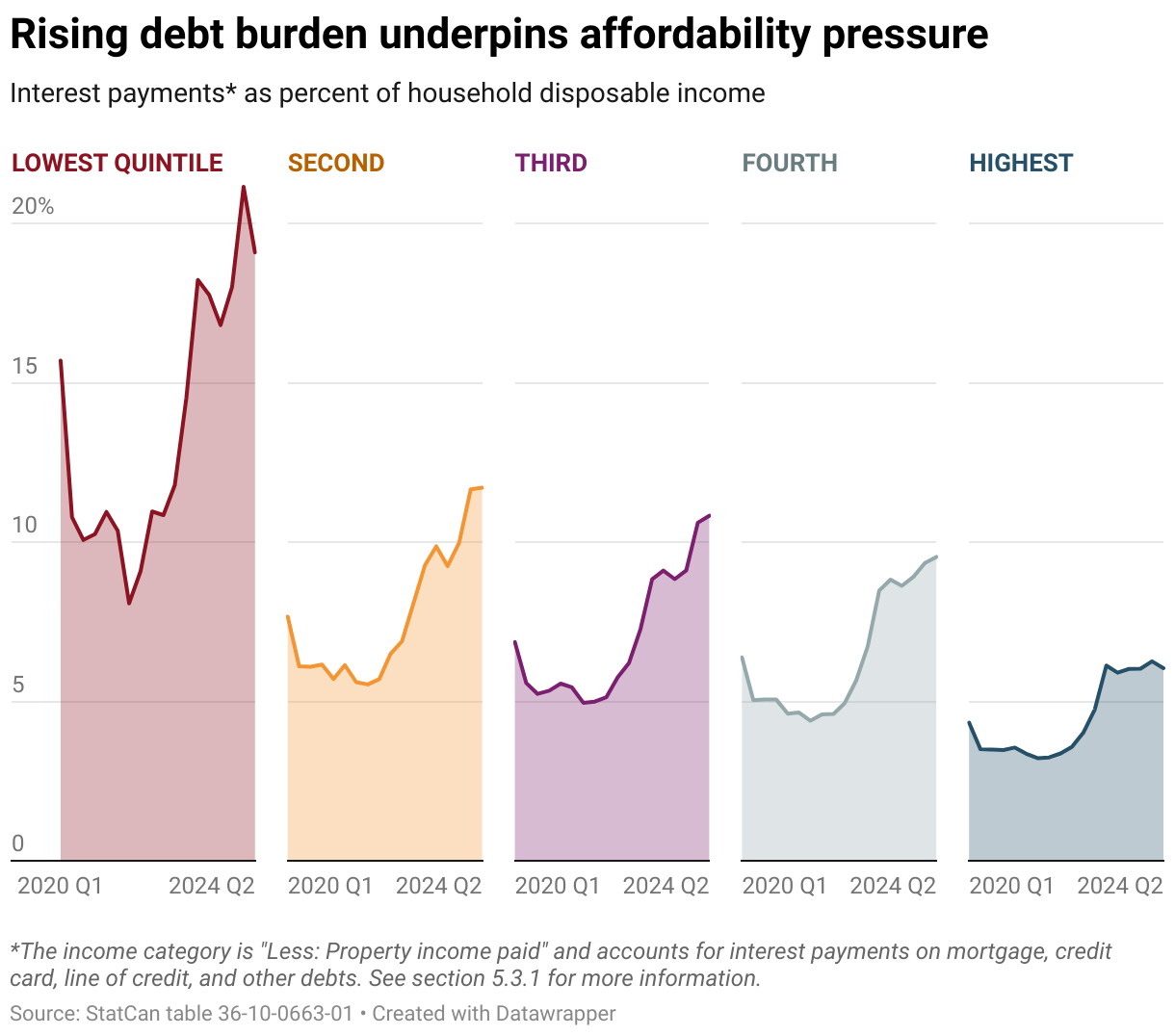

Below, the chart shows the share of disposable income that is taken up just by interest payments on debts, broken down by income quintile. Across all income levels, the share of household disposable income devoted to interest payments on debt increased substantially since the start of 2020.

At the start of 2020, interest payments on debts—such as credit card, line of credit, or mortgage loans—took up an average of about six per cent of household disposable income. By the summer of 2024, that figure had nearly doubled to 11.6 per cent. The impact of debt grows more intense as household income gets lower—it’s especially punishing on the poorest quintile of households, who are paying nearly 20 per cent of their disposable income on interest payments alone.

The rapidly growing pain of debt is the intended consequence of the Bank of Canada’s ill-advised inflation busting strategy, cranking up interest rates to “cool” the economy. It has also made income inequality much worse. Most people are feeling the sting of rising interest rates. However, many high-income households have gained overall from increased investment returns on financial assets due to higher interest rates.

We need a real plan for social and economic justice

The affordability crisis isn’t merely a matter of perception—most households are losing financial ground to debt and the high cost of living. If we are to rise to the moment, we need bold, transformative policy responses—the likes of which are seldom on offer from the political status quo.

Commit to using the power of the Canadian government to forbid corporate price gouging with price controls and tax back windfall corporate profits. It would surely work better than trying to shame corporate executives into lowering prices by bringing them in front of Parliament and asking them stern questions without follow-up.

Burst the housing bubble with strong rent controls and massive build-outs of non-market and co-operative housing, not market-based approaches that only drive prices up.

Transform Canada’s food system by breaking up corporate food sector oligopolies and providing public-sector options in the grocery sector, rather than with toothless, voluntary codes of corporate conduct.

Extend the principles of universality in all vital areas of healthcare including dental, drugs, and mental health, instead of limited, means-tested programs that can be more easily trashed by an incoming government.

Instead of one-time payments to all regardless of need, revitalize income support systems to ensure that nobody ever lives in legislated poverty in Canada ever again.

Cancel all student debts and create stable public funding for post-secondary systems so that tuition can be dramatically lowered and eventually eliminated.

Those were just a few suggestions of what an agenda capable of fighting back against right-wing populism that plays on people’s justified anger and frustration could look like. Real change won’t happen without a mass movement to confront entrenched wealth and corporate power head-on—a movement that many disaffected people who are hungry for a real alternative would be eager to join.

About the author

Ryan Romard

Ryan Romard (He/Him) is a sociologist, research analyst, and data science enthusiast. Ryan has several years of experience conducting survey research in Ontario's public school system and was the CCPA's 2022 Progressive Economics Fellow.