Summary

Retirement security is the dream of every Canadian, but employers, particularly those in the private sector, are moving away from providing the gold standard of a workplace pension plan. In 2023, 6.9 million working Canadians—34 per cent of all employed people—were covered by a registered pension plan. The retirement income those plans contribute to national and local economies, to government budgets and to equalizing retirement security for equity-seeking groups is underappreciated. This report puts that value in context.

Among the report’s findings:

Workplace pension plan payments are major forms of income in Canada: In 2021, workplace pension plans paid out $84 billion in pension payments, accounting for five per cent of all income received by Canadians in that year. Workplace pension plan income was larger in 2021 than all other private retirement income, from Registered Retirement Income Funds (RRIFs), for example. It was larger than all Canada Pension Plan/Quebec Pension Plan (CPP/QPP) income and Employment Insurance (EI) income.

The private sector is bailing on pension plans: While almost all public sector workers with a workplace pension plan have a Defined Benefit plan (the gold standard because it provides the best security). In the 1970s, 90 per cent of private sector workers with a workplace pension plan in Canada had a Defined Benefit plan, similar to the public sector. Today, only 40 per cent of private sector workers with a workplace pension plan have a Defined Benefit plan.

Governments benefit from retirees’ pension income: Across all levels of government, a one-dollar increase in pension income results in governments recouping 41 cents in tax revenue and saved seniors’ supports.

Government contributions to their own workers’ plans provide major returns: In 2023–24, every dollar that governments contributed to their own workers’ pension plans returned $2.38 in higher tax revenue and saved seniors’ supports from retired public sector workers.

Federal coffers benefit from pension income: In total, the federal coffers will be $24.5 billion better off in 2025 due to workplace pension income supporting seniors across the country. This is due to $16.9 billion in additional income tax revenue and $2.3 billion in commodity tax revenue. Pension plan income will also save $1.2 billion in Old Age Security (OAS) and $3.2 billion in Guaranteed Income Support (GIS) payments.

Provincial coffers benefit from pension income: In 2025, provincial governments will see budget balances improved by $16.8 billion due to pension income. The larger provinces of Quebec and Ontario will see $6 billion apiece in improved balances.

Local communities benefit from pension income: Pension income often substitutes for employment income in communities where work is harder to come by. In the top 10 cities where pension income is the most important, employment income is well below the national average. The impact of pension income on all 85 cities and all postal codes can be examined on our interactive pension income map.

Public pensions are a great equalizer: While 90 per cent of women in the public sector have a workplace retirement plan, almost all of which are pension plans, only 44 per cent do in the private sector. For Indigenous workers, 86 per cent have a retirement plan in the public sector, likely a pension, but only 46 per cent do in the private sector and it’s not likely to be a pension. It is a similar story for new Canadians, with 79 per cent having a workplace retirement plan in the public sector but only 45 per cent on the private sector side. There are often right-wing calls to make public sector retirement plans more like those in the private sector. This would be a mistake because it undermines equity goals. Retirement is more secure for women, Indigenous Peoples and new Canadians if they are employed in the public sector.

The goal of government policies should be better retirement security for all. This can certainly be done by encouraging workplace pension plans and by expanding public plans like the Canada Pension Plan (CPP) in the face of employer reticence to provide workplace pensions. Better retirement security through pensions is good for workers, but those workers also play an outsized role in the Canadian economy, in government finances, in ensuring equity for historically disadvantaged groups and in supporting local communities.

Introduction

Workplace pension plans are seen as the gold standard for workers. Unlike other private retirement schemes, like Registered Retirement Savings Plans (RRSPs), a workplace pension plan provides the best security for workers. These plans generally provide better returns since they are professionally managed1 and there is no possibility of outliving one’s retirement savings. Employers are generally obligated to contribute and retirement money in pension plans is more “locked in” than it is in private retirement savings accounts. Moreover, pension plans play an important stabilizing role in markets with their long investment horizons and low leverage.2 3

Defined benefit (DB) workplace pension plans are seen as more desirable because they can shift return shortfalls to the employer. If market returns are below what was needed for the promised benefit, the employer is on the hook for the difference. In reality, even if the employer bears the risk on paper, workers are indirectly risk-bearing parties. If an employer has to put additional money into the plan during an economic downturn, it is surely going to raise those additional costs during wage bargaining. Many large public sector pension plans also share the risk between workers and employers or are jointly sponsored. If there is a plan deficit, both sides have to increase contributions to amortize the deficiency. On top of that, many of these plans have introduced certain plan benefits, such as indexation, that are conditional on returns and not guaranteed. That being said, the DB structure is the most likely to provide a secure and predictable amount in retirement.

While this should be the standard for all workers, it isn’t.

Our publications are available to all at no cost. Please support the CCPA and help make important research and ideas available to everyone.

Make a donation today.

In fact, Canada has been moving further away from this strong retirement option. In part because of this trend and beginning in 2019, the Canada Pension Plan (CCP) and the Quebec Pension Plan (QPP) were enhanced to substitute for the lack of employer pension plans. In the 1960s, governments made a political choice to keep the CPP small—they believed more workers would be covered by better private workplace pension plans over time. Meanwhile, unions argued for a bigger CPP, which has proven to be necessary.

Generally, when we talk about pension plans, the most common one that Canadians will rely on is the Canada Pension Plan or the Quebec Pension Plan. It is one of the key planks for Canadians’ retirement security, with mandatory contributions from both workers and employers. However, unless otherwise specified, this report will focus on the economic impact of private workplace pension plans—the not the public CPP/QPP.

In 2023, 6.9 million working Canadians—34 per cent of all employed people—were covered by a registered pension plan.4 The contribution that beneficiaries of those workplace pension plans make to national and local economies, to government budgets and to equalizing retirement security for equity-seeking groups is underappreciated. This report puts that value in context.

Pension plan income in context

Pension plan payments are major forms of income in Canada. In 2021, pension plans paid out $84 billion in pension payments, accounting for five per cent of all income received by Canadians that year. For comparison, the largest form of income was employment income, which makes up 59 per cent of all income.5

Of the income that pension plans paid out to beneficiaries, the lion’s share comes from public sector plans, which make up 63 per cent of pension payments, worth $53 billion. This goes to workers at all levels of the public sector, from federal, provincial and municipal public administration workers to most educators and health care workers, among others.

The difference of $31 billion in pension plan payments in 2021 came from private sector plans for workers on the private sector side. The private sector is less likely to provide a workplace pension plan than the public sector. An important reason for this is that the private sector has lower unionization rates and one of the key items that unions bargain for is a good retirement plan.

While unionization rates in the public sector have remained relatively stable over the past three decades, they have been falling consistently on the private sector side, going from 21 per cent in 1997 to 16 per cent in 2023.6 In addition to declining unionization, private sector employers have been more aggressively shifting retirement risks onto workers by moving away from Defined Benefit (DB) plans to Defined Contribution (DC) plans or by replacing pension plans with RRSP matching or to nothing at all.

On the public sector side, the attempt has been to switch from DB plans to Target Benefit plans instead of DC plans. Target Benefit plans look like DB plans on the surface: investments are pooled, there is a pension formula, there are age of retirement rules. But, in the end, employer risks are limited and it is permissible to cut pension benefits, even to retirees, in the face of a shortfall.

While almost all public sector workers with a pension plan have a Defined Benefit plan, the situation has changed substantially for private sector workers in the past half century. In the 1970s in Canada, 90 per cent of private sector workers with a pension plan had a DB plan, similar to the public sector. Today, only 40 per cent of private sector workers with a pension plan have a DB plan, as shown in Figure 1. A common approach to the downgrading of private sector worker retirement benefits is to maintain higher-quality plans for older workers but shift younger employees to lower-quality plans or cut them off entirely. These retirement security downgrades have received stiff opposition from the unions representing those workers, sometimes resulting in improved retirement security for younger workers in subsequent agreements.7

Compared to other major income sources, pension plan payments are often more important to Canadians than many would recognize. Figure 2 compares public and private sector pension plan payments to other similarly sized income flows at the aggregate level. For instance, pension payments from public sector pensions alone are larger than all Employment Insurance (EI) and all Old Age Security (OAS) payments. Pension payments from public sector plans are roughly equivalent to all other forms of private retirement income—for example, withdrawals from RRIFs (what RRSP savings become after age 65).

When we combine public and private pension payments, they contributed more to income than the Canada Pension Plan/Quebec Pension Plan or from all self-employment income in 2021. The CPP/QPP was received by more people, but pension plan payments contributed more to incomes in Canada.

There is often plenty of focus on entrepreneurship and how to encourage it but, generally speaking, it’s not associated with retirement security: self-employment income is a smaller source of income than pension payments.

Pension plan revenues8

The ultimate source of pension payments is often thought to be the contributions that workers and employers make during one’s working years. Workers forgo earnings in their working years that could be spent in the economy in order to have security in their retirement years. Those retirement dollars are then spent in the economy but after one’s working life.

However, most pension plan revenues don’t come from contributions, as shown in Figure 3. Worker and employer contributions only make up a third of pension plan revenues. Employers and workers only contributed 14 per cent and 18 per cent, respectively, to pension plan revenues in 2023–24.9 Investment income—in the form of interest and dividend payments—was the biggest revenue source that year, accounting for 36 per cent of revenue. Profits from the sale of investments made up 26 per cent of revenue. In other words, investment income and equity returns are the main source of benefits in retirement, making up two thirds of the benefit value.10

The Healthcare of Ontario Pension Plan (HOOPP) calculates that all contributions made by workers are returned as benefits within the first four years of retirement, with all remaining benefits due to investment returns.11

When it comes to that minority revenue source of contributions, much attention is paid to the relative split between what employers and workers are contributing. In the public sector, as shown in Figure 4, the ratio is slightly in favour of workers, but not by much. Workers in public sector plans contribute 46 per cent of contributions while employers contribute the other 54 per cent.

While much attention is focused on making the split 50/50 in the public sector, the situation of private sector plans is rarely examined. In fact, for private sector plans, it’s the employer that makes up the lions’ share of contributions, at 68 per cent, as shown in Figure 5. Workers only contribute 24 per cent of total contributions.

Among the plans where only the employer contributes, 99 per cent of them are private sector plans.12 Some of these are flat-benefit DB plans, with the private sector paying a modest pension without indexing or early retirement provisions.

Substantial differences in compensation between public and private sectors at the high end also play a role in this larger employer contribution for private sector plans. High-end salaries in the private sector are incomparable, with more modest salaries in the public sector, even for workers of similar characteristics.13 The types of salaries available to Bay Street or oil executives are miles higher than what’s possible even in the highest echelons of the public sector. High-income private sector workers often have pension plans where the employer contributes much more, skewing the results. Having a large, mostly employer-funded pension plan is a perk of executive positions in the private sector that doesn’t exist in the public sector.

Right-wing commentators will often argue that the public sector should be more like the private sector when it comes to pension contributions. But if we wanted to make public sector pensions more like private ones, it would mean that governments should be contributing a lot more to pension plans, and/or workers contributing far less, particularly for highly paid public sector managers.

Pension plans and government coffers

Given its importance as an income source, it should come as no surprise that changes in this income type have measurable impacts on government coffers. Pension income, when it is received, is taxable income. As well, much of pension income is spent on goods and services.

Changes in pension income will also impact government coffers. Pension income is taxable—just like income taxes—and indirectly through commodity taxes when spent. Moreover, seniors’ income supports are the largest category of income support programs, particularly for the federal government. The impact of changes to pension income will be felt on both the federal and provincial levels, which provide commodity and seniors’ income supports (although provincial seniors’ supports are much smaller).

To better understand these impacts, Statistics Canada’s tax modelling software, the Social Policy Simulation Database and Model (SPSD/M 30.1), was used in this study. Within the model, pension income was increased and decreased by various percentages to determine how all federal and provincial tax and transfer programs would react. The per-dollar effects were quite similar and symmetrical, regardless of the percentage change, which ranged from -15 per cent to +15 per cent. Table 2 illustrates the impact on various government lines per one dollar increase and per one dollar decrease in pension income.

If pension income rises by one dollar, federal government finances improve by 24 cents, whereas provincial governments finances improve by 17 cents.

At the federal level, that one-dollar increase in pension income causes an 18-cent increase in income taxes, since pension income is taxable. It also contributes to a two -cent increase in commodity taxes from sources like the Good and Services Tax/Harmonized Sales Tax (GST/HST). In addition, federal transfers fall by four cents. This is due mostly to lower Old Age Security (OAS) and Guaranteed Income Supplement (GIS) payments, as those are clawed back against additional pension income.

The situation is broadly similar at the provincial level, although to a lesser extent because provincial taxation income represents a smaller share. As pension income rises by a dollar, the provinces take in an additional 12 cents in income taxes because pension income is taxable at both the federal and provincial levels. The provinces also have commodity taxes, like Provincial Sales Tax (PST) or the provincial portion of HST. That additional dollar of pension income results in three cents of higher provincial commodity taxes—slightly more than the federal government gets from pension income changes on its commodity taxes. The provinces do have senior income supports, but they are much smaller than federal supports. As pension income rises by a dollar, the provinces save a penny in senior supports.

If pension income falls by a dollar, we see roughly symmetrical effects. The federal government sees a 24-cent deterioration in its finances. This breaks down to a loss of 18 cents from income taxes and two cents from commodity taxes as people spend less due to reduced pension income. Federal transfers, via Old Age Security (OAS) and Guaranteed Income Security (GIS), automatically rise by four cents to support those seniors with lower pension income.

The provinces also see an impact if pension income declines by a dollar: Provincial finances deteriorate by 17 cents. Of that total, 13 cents of the loss comes from lower income taxes and three cents comes from lost commodity taxes. Provincial income supports for seniors rise by a penny to slightly offset the one-dollar decline in pension income.

Unlike private sector employers, governments both contribute to pension plans and reap direct financial benefits through taxation.

Often governments think of their contributions to pension plans as costs. However, they are also a substantial source of income when public sector workers draw on their pension after retirement. For a single worker, governments only see expenditures during their working life, but upon retirement, that translates into pure revenue for governments via taxation.

We can calculate the direct financial benefit to governments due to their pension contributions at this point in time. Governments only contribute 17 per cent of the revenue of public pension plans, as noted above. Public sector workers contribute 15 per cent of revenue, but in 2023–24, the lion’s share came from the return on investment, either through dividends and interest or through the sale of assets at a profit. In essence, a 17-cent government contribution to public pension plans yields $1 in pension income.

This analysis overestimates the contributions of federal and provincial governments in public sector pension plans because it includes the contributions of municipal governments on behalf of their workers. Municipalities, like private companies, don’t have taxation power over income and so don’t directly benefit from pension income paid out to retirees.

In Table 2, we see that every dollar in pension income generates 41 cents in government tax revenue or saved seniors’ supports. Therefore, for every dollar governments contribute to the pension plans of their workers they receive $2.38 in taxes and savings in senior’s supports. Broken down a little, for every dollar that governments invest in pension contributions, they save 30 cents in income supports they don’t have to pay. They gain 30 cents back in commodity taxes and they gain a tremendous $1.78 in income taxes.

These high rates of returns for federal and provincial contributions are underestimated because municipalities are major contributors to public sector pension plans, which are included on the public sector contributions side. Yet these higher levels of government are the ones that directly benefit from pension income when it’s paid out—cities don’t.

The above sections examine returns to governments per dollar of pension income. Those dollars add up to billions. Table 3 shows the projected 2025 impact of pension income on federal government coffers. In 2025, pension income is expected to generate $16.9 billion in income tax revenue. The federal government will save an additional $1.2 billion in OAS payments and $3.2 billion in GIS payments. When combined with other income support programs that kick in if seniors’ incomes plummet, the federal government would save $5.2 billion in income support programs. The federal government would also rake in $2.3 billion in commodity taxes, such as the GST, as seniors spend their pension income.

In total, the federal coffers will be $24.5 billion better off in 2025 due to workplace pension income supporting seniors across the country.

Across all levels of government, a one-dollar increase in pension income results in governments recouping 41 cents.

Provincial governments are also major beneficiaries of pension income over and above what the federal government takes in. In 2025, provincial governments will see budget balances improved by $16.8 billion due to pension-related revenue. The larger provinces of Quebec and Ontario will see the largest gains. Each will receive over $4 billion in 2025 by taxing pension incomes. Each will have income transfer payments that are three quarters of a billion dollars lower due to pension income. Quebec and Ontario will rake in a further $899 million and $1.4 billion, respectively, in 2025 from commodity taxes based on pension income being spent.

Pension income is a boon for both federal and provincial governments, returning at least a dollar for every dollar they contribute.

These estimates of returns to governments don’t include the benefits that pensions provide to the broader economy. Ontario Municipal Employees Retirement System (OMERS) is estimated to create $16.4 billion in economic activity in 2023 for every $10 billion that is paid to its retirees.14

These economic benefits are in addition to the benefits to actual workers who contribute much less to achieve the same results. The private savings retirement model, such as a RRSP, generates $1.70 in retirement income for every dollar invested. However, that same dollar invested in a pension plan returns $5.32 in retirement income.15

Pension plan coverage and identity

Better understanding the characteristics of workers who have a workplace pension plan can provide insight into the possible equity impacts on workers if pension plans change. The Labour Force Survey (LFS) combines both workplace pension plan access and socio-demographic variables.

The LFS asks workers about various employment benefits that they receive. One of the benefits options is the presence of a workplace pension plan. However, there are no other retirement-benefit type options among the choices. As a result, workers are likely including any retirement benefits as workplace pension plans even if they aren’t strictly workplace pension plans. In 2023, the LFS concludes that 8.4 million workers say their job provides a workplace pension plan,16 but there were only 6.9 million active members of pension plans.17

What’s likely happening is that respondents are including all retirement benefits—such as employer-matched RRSPs or Pooled Registered Pension Plans (PRPPs)—as “workplace pension plans” because there are no other choices provided in the LFS. Nonetheless, the LFS can be an important data source to understand who has access to workplace retirement benefits and who doesn’t. We can examine pension membership by gender, Indigenous identity and immigration status. Unfortunately, due to data constraints, this analysis could not be extended to racialized workers.

The results are presented in Figure 6, which examines the proportion of workers who have access to workplace retirement (public and private sector) according to their identity.

It’s worth understanding that the public sector is more likely to hire women than the private sector. This is also the case for all three Indigenous identities of First Nations, Métis and Inuit peoples. Recent immigrants are more likely to work in the private sector.

Public sector workers are far more likely to have a workplace retirement plan and it’s almost always a pension plan. In the private sector, half of workers have some form of workplace retirement plan, but that is more likely to be a savings plan, such as RRSP matching, that shifts retirement risk to the worker.

The net result of these trends is that historically disadvantaged groups are much more likely to have a workplace retirement plan in public sector employment and that plan is much more likely to be a pension.

While 90 per cent of women in the public sector have a workplace retirement plan, almost all of which are pension plans, only 44 per cent of them have a retirement plan in the private sector. And even if they do, not likely to be a pension.

For Indigenous workers, 86 per cent have a retirement plan in the public sector, likely a pension, but only 46 per cent have a retirement plan in the private sector and it’s not likely to be a pension.

It is a similar story for recent immigrants, with 79 per cent having a workplace retirement plan in the public sector but only 45 per cent on the private sector side.

There are often right-wing calls to make public sector retirement plans more like those in the private sector. This would be a mistake because it undermines equity goals. Retirement is more secure for women, Indigenous Peoples and new Canadians if they are employed in the public sector. From an equity perspective, Canada shouldn’t seek to reinforce inequities among historically disadvantaged workers by eliminating their retirement security. Canada doesn’t need a race to the bottom, it needs better retirement security for all workers.

Pension income and local communities

Where pension contributions are being paid by workers isn’t necessarily where pension income is being paid to retirees. This can be due to retirees moving upon retirement and taking their pension dollars with them. It can also be due to historical reasons. For instance, if a community used to have a unionized factory that has since closed, there may be plenty of retired pension recipients but far fewer pension contributors in that community today.

To examine this further, we compare the workers contributing to pension plans to those receiving income from those pension plans and look for mismatches. Figure 7 does this by comparing pension payment to the count of unionized workers in each Forward Sortation Area (FSA), which represents the first 3 digits of a postal code. Unionization is no guarantee of a pension, but it certainly makes it much more likely. The counts of workers contributing to a pension plan are difficult to obtain via postal code, so unionization is used as a proxy for pension contributions in this study.

If we examine mismatches by community size, we find that 2.2 per cent of unionized workers live in rural postal codes but 2.7 per cent of registered pension plan income is paid in those postal codes. The result is that pension income is 22 per cent higher than the count of unionized contributors in these areas.

A similar result is found for villages and towns with fewer than 100,000 people, where pension income received is higher than the count of unionized workers likely contributing to pension plans.

In cities of over 100,000 people, there are more unionized workers likely contributing to pension plans than there is pension plan income paid: 65.6 per cent of unionized workers live in cities but only 59.7 per cent of pension income is paid to retirees there.

No matter the reason for the mismatch between workers contributing to and retirees drawing from a pension, smaller town and rural areas seem to benefit the most. They see net more income flowing in from retiree income than they see being withdrawn from contributions.

Beyond comparing contributions to pension income by community, we can also examine which communities are reliant on registered pension income. Table 5 shows the top 10 of 85 cities that are the most reliant on registered pension income in 2021. Each city has at least seven per cent of its income derived from pension income, which is well above the national average of 4.9 per cent. The full list of 85 cities sorted by registered pension income reliance is available in the appendix.

In seven of these cities, pension income is more important than other similarly sized income flows. For instance, in the regional municipality of Cape Breton, registered pension income comprises 7.6 per cent of all income. All other private retirement income, from sources like RRIF withdrawals, make up 5.3 per cent of all income. Self-employment or entrepreneurial income make up 2.7 per cent and government benefits income (from programs like EI and social assistance) makes up 11.6 per cent of all income.

In most of these top 10 communities, employment income makes up a notably lower contribution to total income than the national average of 59 per cent. For instance, in Shawinigan, employment income only makes up 52 per cent of all income.

Consistently lower employment income in these communities suggests that registered pension income can be an important support to sustain demand for local goods and services, especially if local employment is hard to come by.

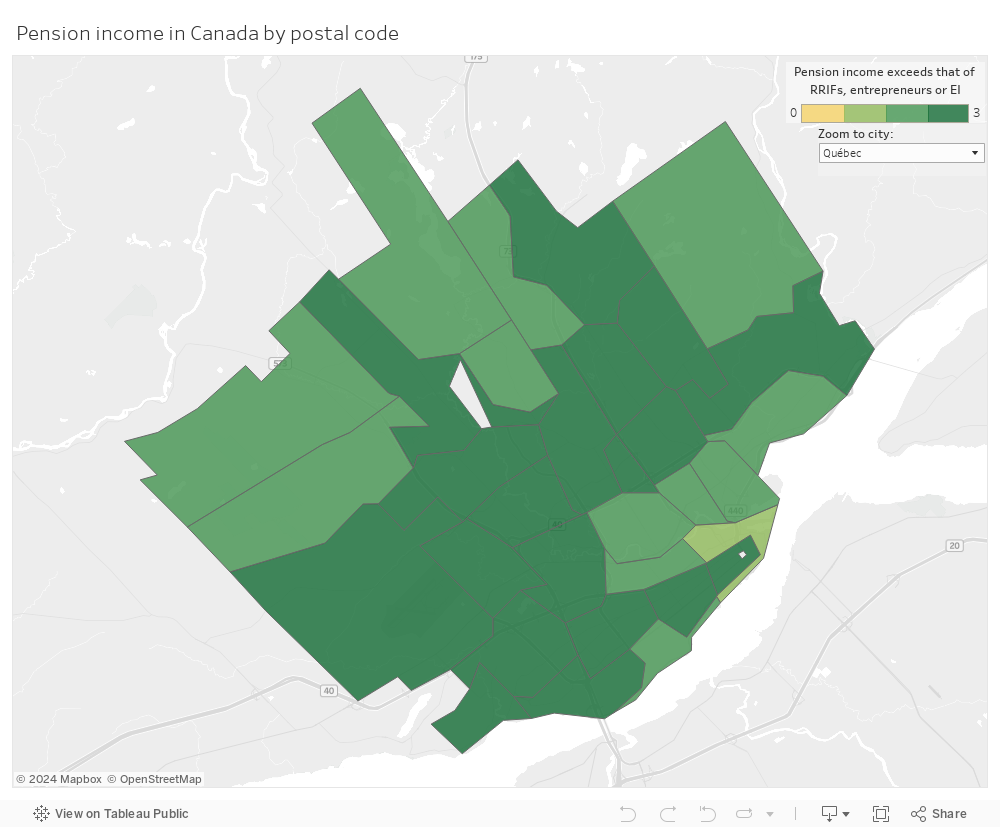

The importance of pension income can be traced further down to the postal code level, as illustrated in Figure 8, which examines Quebec City and its constituent postal codes. Quebec City is the most reliant of Canada’s large cities on pension income: 6.5 per cent of its income is pension income, well above the national average of 4.9 per cent.

While Figure 8 examines Quebec City, any postal code or any big city can be examined using our online pension map. For each postal code, the user can see how much registered pension income was paid in 2021 and compare that to other similarly sized income types.

In the case of Quebec City, in 21 of the 32 postal codes, registered pension income is larger than all other withdrawals from private retirement savings—larger than entrepreneur self-employment income and larger than government income supports from programs like EI and social assistance.

In more of the downtown areas of the city, as well as the more rural areas on the outskirts, pension income ranks second (usually following government benefits like EI and social assistance). However, in the suburbs, more central for the city’s land mass, pension income beats out the other income types examined.

These geographic trends are hardly universal; it merits further examination to determine where pension income provides the most impact to local economies.

Conclusion

Workplace pensions are often viewed as a benefit solely to those receiving them. Certainly, workplace pensions benefit the workers themselves through a much more secure retirement. However, pension income built on investment and equity returns over decades makes up an important part of Canadians’ income and is an important source of income support for many local communities.

The goal of government policies should be better retirement security for all. This can certainly be done by encouraging workplace pension plans and by expanding public plans like the CPP in the face of employer reticence to provide workplace pensions.

Better retirement security through pensions is good for workers, but those workers also play an outsized role in the Canadian economy, in government finances, in ensuring equity for historically disadvantaged groups and in supporting local communities.

Appendix 1: Methodology

One of the challenging aspects of examining pensions is obtaining proper data on income paid out from private pension plans outside of CPP and disaggregated from other forms of private retirement income, like RRIF withdrawals. These are aggregated on line 11500 of the income tax form in a general private retirement income line. The line certainly includes workplace pension plans, but it also includes all other forms of private retirement income, from RRIF withdrawals, PRPP payments and the like. Therefore, utilizing T1 based datasets, like the T1 Family File (T1FF), won’t be useful in obtaining private pension plan income because it is already aggregated on the T1. Data experts at Statistics Canada confirmed we could not obtain only RPP payments to tax filers as a result. Line 11500 of the T1 is readily available and used extensively in this report, but it is not specific enough as is to isolate the income from RPPs only.

There are two other Statistics Canada surveys that examine pension plans in Canada: The Quarterly Estimates of Trusteed Pension Funds (QTPF)18 and the survey of Pension Plans in Canada.19

The QTPF has detailed revenue and expenditure data, including pension payments paid out to pension recipients, which is one of the key data points required for this analysis. Unfortunately, not all registered pension plans (RPPs) are trusteed pension funds (TPFs). There are RPPs, particularly for private sector employers, that aren’t overseen by a board of trustees. Therefore, while the data from the QTPF is incredibly useful, it doesn’t represent the full universe of RPPs in Canada.

The survey of Pension Plans in Canada does cover all RPPs, but it contains no details on fund expenditures generally or amounts paid out to beneficiaries in particular. It does contain employer and employee contribution amounts on an annual basis. This overlapping data is also available in the QTPF.

Therefore, we can match up the two surveys and compare their estimates of contributions to determine what proportion the TPF represents of the complete universe of Canadian pension plans. In 2021, 97 per cent of the income from the QTPF for public sector employers are included in the broader RPPs universe. In other words, the QTPF represented basically all registered pension plans on the public sector side. On the other hand, private sector contributions from the QTPF made up 62 per cent the broader RPP universe in 2021. On the whole, across public and private sector employers, the QTPF contributions data makes up 86 per cent of the contributions of all RPPs.

The two surveys also both contain estimates of the market value of assets. We see similar ratios of the QTPF to the full RPP universe for both public and private sector plans. In 2021, the QTPF reports 99.6 per cent of all the market value of assets for public sector funds reported in the RPP survey. For private sector plans, the QTPF reports 67 per cent of the market value of assets reported in the broader RPP survey. Combining both public and private sector plans, the QTPF includes 90 per cent of the market value of assets reported in the broader RPP universe.

Given these relationships, and assuming the pension payments have similar ratios, it is possible to gross the QTPF statistics to estimate all RPP income paid, with ratios of 102.67 per cent for public sector pension payments and 160.89 per cent private sector pension payments.

These broad estimates are then used to pull out the registered pension plan payments from line 11500 at lower levels of geography.

This approach makes several implicit assumptions that may not be true. First, it assumes that differences between QTPF contributions and RPP contributions are similar to differences between QTPF pension payments and those of broader RPP pension payments. Second, it assumes a stable relationship between RPP pension payments on line 11500 at provincial and FSA geographic levels. These may well be violated, but no better data sources exist.

In this report, all estimates in this report of RPP pension payments use the above methodology unless otherwise noted. However, there are sections that have detailed comparisons between pension plan expenditures and revenues. Those sections rely exclusively on the QTPF data as largely representative of the broader RPP universe.

Notes

- David Dodge, “Economic and Financial Efficiency: The Importance of Pension Plans”, remarks to l’Association des MBA du Québec (AMBAQ), Montréal, Quebec, November 2005, https://www.bankofcanada.ca/2005/11/economic-financial-efficiency-importance-pension-plans/.

- Lawrence L. Schembri, “Double Coincidence of Needs: Pension Funds and Financial Stability”, remarks to Pension Investment Association of Canada, May 2014, https://www.bankofcanada.ca/2014/05/double-coincidence-needs-pension-funds/.

- Guillaume Bédard-Pagé, Annick Demers, Eric Tuer and Miville Tremblay, “Large Canadian Public Pension Funds: A Financial System Perspective”, Bank of Canada, Financial System Review, June 2016, https://www.bankofcanada.ca/wp-content/uploads/2016/06/fsr-june2016-bedard-page.pdf.

- Total employed, all classes/total of registered pension plans active members. From Statistics Canada. Table 14-10-0027-01 Employment by class of worker, annual (x 1,000) and Statistics Canada. Table 11-10-0097-01 Registered Pension Plans (RPPs), active members and market value of assets by type of organization.

- Canada Revenue Agency, “T1 Final Statistics: Table 5: All returns by province and territory of residence”, 2021 tax year, https://www.canada.ca/en/revenue-agency/programs/about-canada-revenue-agency-cra/income-statistics-gst-hst-statistics/t1-final-statistics/2021-tax-year.html.

- Statistics Canada. Table 14-10-0070-01 Union coverage by industry, annual (x 1,000).

- See for instance autoworkers being shifted from a DC plan back to a DB plan. “GM, Unifor agreement includes transition to CAAT DBplus pension plan, benefits gains”, Benefits Canada, October 7, 2024, https://www.benefitscanada.com/benefits/health-benefits/gm-unifor-agreement-includes-transition-to-caat-dbplus-pension-plan/.

- The most detailed expenditure and revenue data for pension plans are only available for Trusteed Pension plans through the quarterly Trusteed Pension Fund (TPF) survey. See the appendix for a comparison of the TPF and RPP survey data.

- Statistics Canada. Table 11-10-0086-01 Trusteed pension funds, revenues, expenditures and net income, quarterly (x 1,000,000).

- These ranges of comparisons are common for individual funds as well, See for instance: Ontario Pension Board, “Contributing to the plan: How do contributions work?” https://www.opb.ca/current-mem...

- Healthcare of Ontario Pension Plan (HOOPP), “How your pension works: What you put in vs what you get out”, https://hoopp.com/members/hoopp-pension-features/pension-calculation.

- Statistics Canada. Table 11-10-0114-01 Registered Pension Plans (RPPs), active members and market value of assets by employee contribution rate.

- David Macdonald, “How the public sector is fighting income inequality (and why it's still not enough)”, February 2024, Canadian Centre for Policy Alternatives, https://policyalternatives.ca/publications/reports/how-public-sector-fighting-income-inequality-and-why-its-still-not-enough.

- Smetanin, P., Stiff, D., OMERS and its Members: Ontario Economic Contribution 2023. Canadian Centre for Economic Analysis. December 2023, https://assets.ctfassets.net/iifcbkds7nke/5UoHxzz8a6RXvLoAcoWK3t/38679e81d4309b1f012da1ce5b075935/2023_Economic_Contributions_of_OMERS_and_its_Members_in_Ontario-ua.pdf.

- Healthcare of Ontario Pension Plan, “The Value Of A Good Pension: The business case for good workplace retirement plans“, 2021, https://hoopp.com/docs/default-source/newsroom-library/research/vgp-the-business-case-for-good-workplace-retirement-plans.pdf

- Statistics Canada, Custom tabulation, Labour Force Survey.

- Statistics Canada. Table 11-10-0097-01 Registered Pension Plans (RPPs), active members and market value of assets by type of organization

- Quarterly Estimates of Trusteed Pension Funds (QTPF), Standards, datasources and methods, Statistics Canada, https://www23.statcan.gc.ca/imdb/p2SV.pl?Function=getSurvey&SDDS=2607

- Pension Plans in Canada, Standards, datasources and methods, Statistics Canada, https://www23.statcan.gc.ca/imdb/p2SV.pl?Function=getSurvey&SDDS=2609.

Acknowledgements

The author would like to thank the following reviewers of an earlier draft of this paper for their comments: Patrick Imbeau, Mark Janson, Troy Lundblad and Chris Roberts. Also, thanks for Ryan Heasman for his invaluable research assistance.

About the author

David Macdonald

David joined the CCPA as its Senior Ottawa Economist in 2011, although he has been a long time contributor as a research associate. Since 2008, he has coordinated the Alternative Federal Budget, which takes a fresh look at the federal budget from a progressive perspective. David has also written on a variety of topics, from child care to income inequality to federal fiscal policy. He is a regular media commentator on national policy issues, often speaking to the CBC, Globe and Mail, Toronto Star and Canadian Press. David received his BA from the University of Windsor and his MA from the University of Guelph, both in Philosophy. Follow David on Bluesky at @davidmaccdn.bsky.social